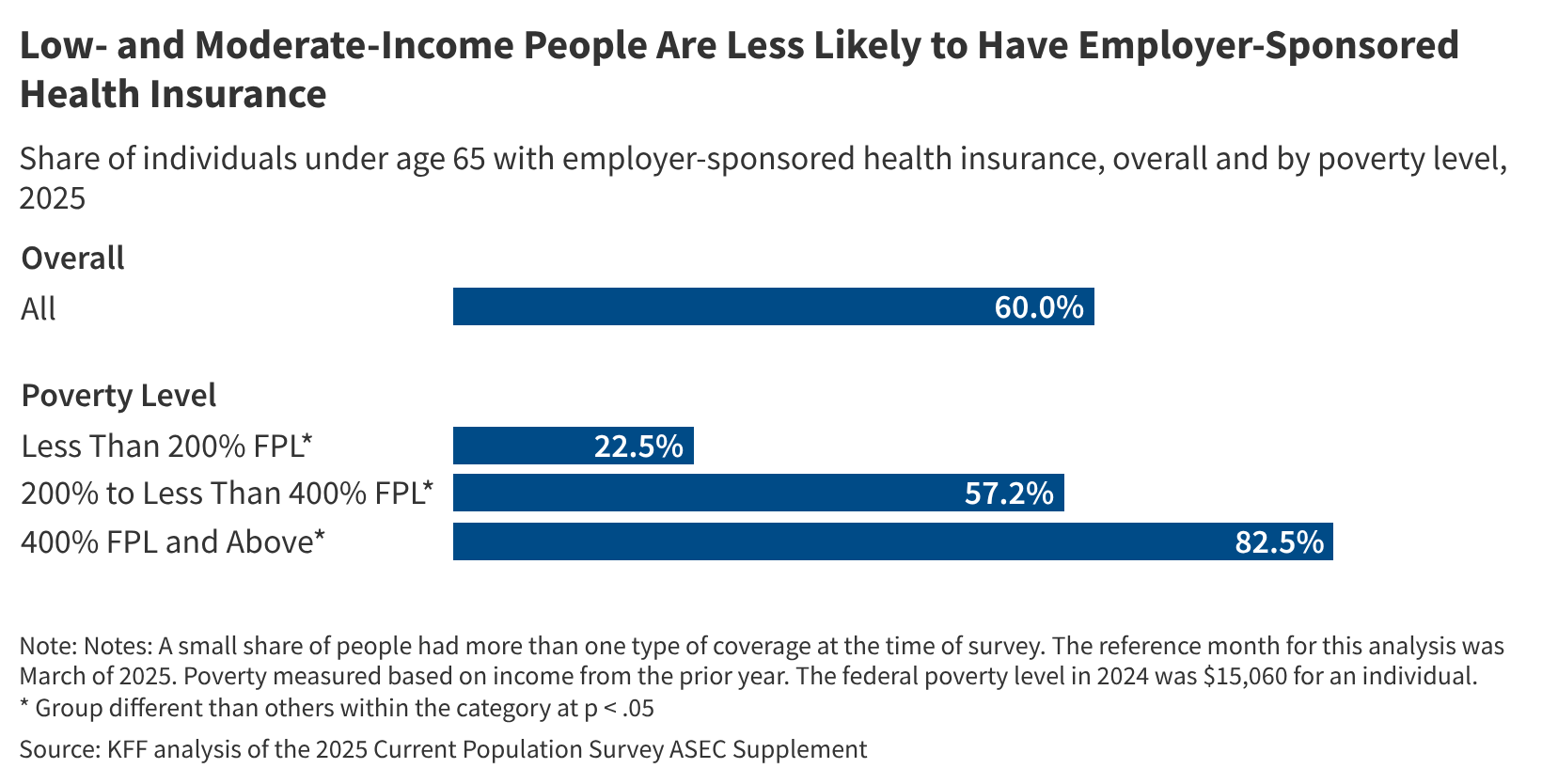

Employer-sponsored health insurance remained the dominant source of coverage in the U.S. as of March 2025, reaching 165.6 million people under age 65, according to new KFF data. Four in five adult workers under 65 (80%) were employed by a company that offered health insurance to at least some employees. That share fell sharply for lower-paid workers, only 60% had access. Uptake was even more unequal: just 22.5% of those earning below 200% of the federal poverty level were covered through an employer, compared with 82.5% among those above 400%. The analysis, based on the March supplements of the Current Population Survey, was released through the Peterson-KFF Health System Tracker series.

Employer coverage continues to anchor the private U.S. insurance landscape, yet the disparities are deepening. High-income households are maintaining steady access while lower-income workers remain priced out or left without an offer. For payers and benefits consultants, this signals a divided market, large employers sustaining comprehensive plans with stable risk pools, smaller or lower-wage firms falling further behind. And for PBMs and plan administrators, the rise of uninsured low-wage workers is more than a statistic; it’s a political spark. If exchange premiums and deductibles stay elevated, calls for affordability fixes or a new public option will only grow louder. See related analysis at RxBenefits.ai.

Some analysts view this as a ceiling for employer coverage. Offer rates in lower-wage industries have stalled, and new coverage gains will come only from subsidy expansion or public alternatives, not a sudden surge in employer generosity. Investors should watch retail and service employers closely heading into 2026 renewals, some may re-enter sponsorship to compete for labor, others might quietly step away. Even small shifts now can move millions of people, given the base size of 165 million. The KFF numbers make the pattern plain: coverage expansion headlines hide a distribution crunch. And the next phase of health reform? Less about who gets in, more about who can afford to stay there. That’s the uncomfortable truth the data won’t let anyone ignore.

![<![CDATA[CAQH Index Finds $20 Billion in Cost Savings Opportunities]]>](https://images.builtfor.ai/images/article-images/cdata-caqh-index-finds-20-billion-in-cost-savings-opportunit.jpg)