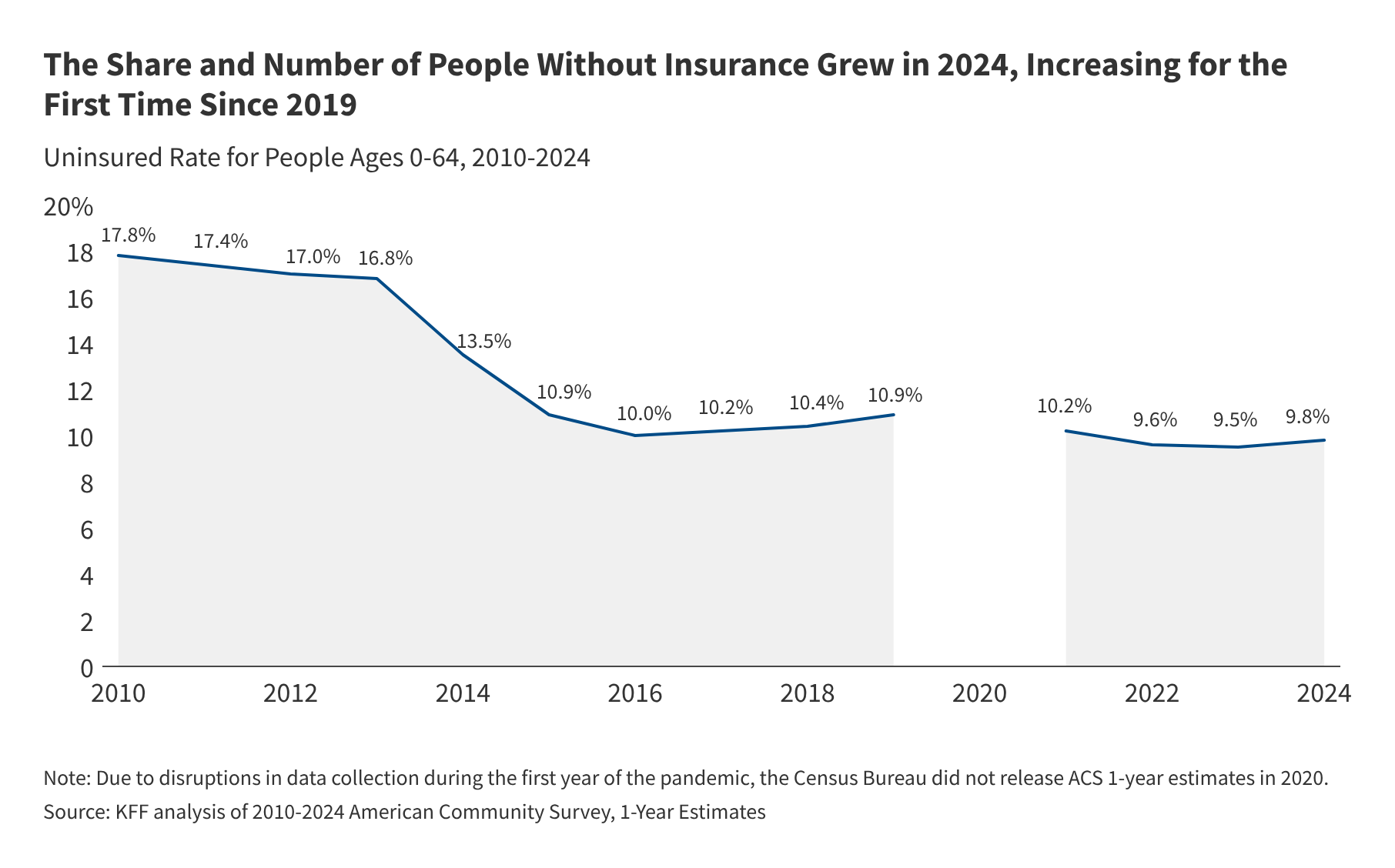

New analysis from KFF Health News, published April 9, 2026, shows that the number of uninsured Americans under age 65 rose by more than 1.3 million in 2024 to reach 26.7 million. That marks the first uptick in the uninsured rate since 2019. The rate climbed from 9.5% to 9.8%, driven mainly by a drop in Medicaid coverage after the continuous enrollment policy ended in 2023. Nearly all states finished Medicaid eligibility redeterminations by the end of 2024, and millions lost coverage. Enrollment in ACA Marketplace plans did rise, but not enough to offset the Medicaid decline. KFF found that over 80% of the uninsured are in low-income families, about 85% live in households with at least one worker, and most reside in states that have not expanded Medicaid under the ACA.

The data show that post-pandemic Medicaid unwinding and changing policy are reshaping the U.S. coverage landscape in real time. The rollback of continuous enrollment and the upcoming expiration of enhanced Marketplace subsidies, triggered by the 2025 reconciliation law, are on track to drive further coverage erosion. The Congressional Budget Office projects that over 14 million additional people will be uninsured by 2034 if current policies hold. For payers and providers, that shift signals heavier uncompensated care loads and sicker patients in safety-net settings. On the financial side, PBM economics and provider reimbursement will be pulled toward greater noncommercial exposure as Medicaid declines faster than private coverage expands. A subtle but consequential rebalancing.

Viewed another way, the reversal looks like an early warning for state budgets and hospital margins through 2026 and beyond, especially in non-expansion states. With federal subsidies likely to wane, Marketplace affordability gaps are widening and may soon define the next policy flashpoint. Premium assistance and state-based subsidies are becoming contested ground. Investors should keep a close eye on how state coverage experiments interact with federal policy because those interactions will set the tone for payer enrollment and bad-debt risk across the health system. And honestly, after watching these cycles for years, this feels less like a one-year blip and more like the start of another slow unwind.

![<![CDATA[CAQH Index Finds $20 Billion in Cost Savings Opportunities]]>](https://images.builtfor.ai/images/article-images/cdata-caqh-index-finds-20-billion-in-cost-savings-opportunit.jpg)