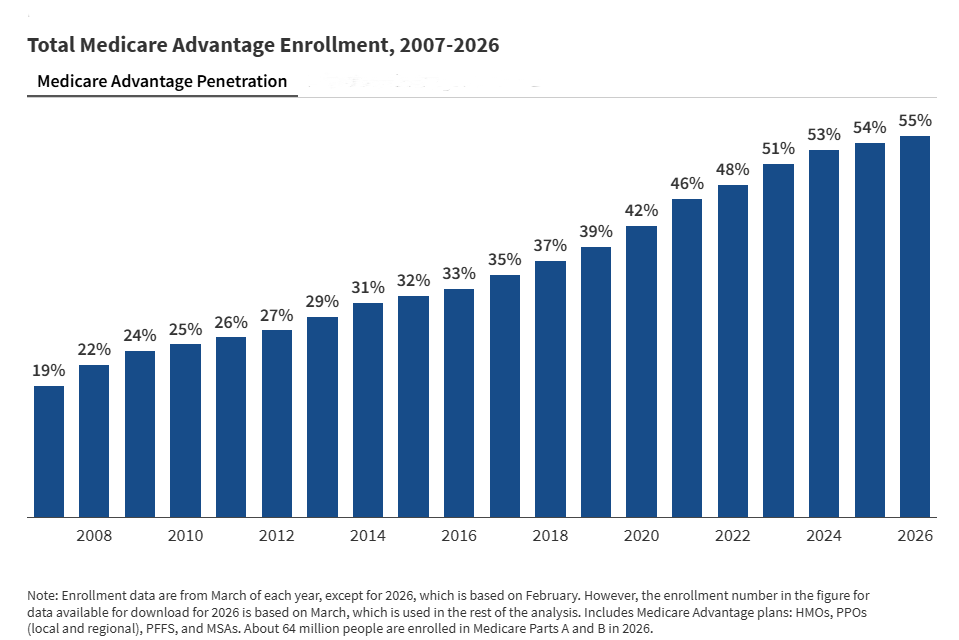

Enrollment in Medicare Advantage climbed to 55% of eligible beneficiaries in 2026, roughly 35 million of the 64 million people covered under Medicare Parts A and B, according to new KFF analysis. Per-person payments to private Medicare Advantage plans average 14% above comparable spending in traditional Medicare, adding about $76 billion to federal costs this year alone. Nearly one quarter of enrollees (23%) now belong to special needs plans (SNPs), which accounted for 85% of net enrollment growth from 2025 to 2026. More than three-quarters of SNP members are in dual-eligible (D‑SNP) products, while chronic-condition SNPs (C‑SNPs) jumped 45% year over year and now represent 20% of all SNP participation. UnitedHealth Group and Humana remain the industry’s dominant players with a combined 46% share, but their trajectories diverged: UnitedHealth slipped to 26% (from 29%), while Humana advanced to 20% after adding 1.3 million members as UnitedHealth shed roughly 647,000.

The program’s sheer scale has turned Medicare Advantage into the core of U.S. retiree risk-bearing, and a moderating growth rate signals that the market is bumping up against saturation rather than losing appeal. With more than half of Medicare beneficiaries in private plans, policymakers are under growing pressure to reconsider program financing. Those 14% higher payments, equal to $76 billion in extra federal spending, have drawn mounting scrutiny from MedPAC and congressional staff, yet no clear reform path has emerged. Any realignment will test the balance between fiscal restraint and the political weight of supplemental benefits like dental, vision, and hearing coverage. Nobody wants to be the lawmaker who trims popular perks for seniors.

For investors and insurers, these numbers reshape the competitive picture. Humana’s rebound after several years of share slippage suggests its renewed focus on higher-acuity populations through D‑SNPs and C‑SNPs is working. UnitedHealth’s contraction may signal portfolio cleanup or cautious repricing ahead of tighter rulemaking. If Washington moves to narrow the 14% payment gap with fee‑for‑service Medicare, growth strategies built on the current margin will feel the strain. Keep an eye on upcoming CMS actions and MedPAC recommendations later in 2026, they’ll indicate how fast policymakers want to move. The story’s not finished, but the trend lines are clear. For employer and retiree plan benchmarking, see RxPBM.ai.